1. Overview

Against the backdrop of deepening medical infrastructure development, the decentralization of high-quality medical resources, and the widespread adoption of minimally invasive surgery, the endoscope—as a core tool for clinical diagnosis and treatment—is witnessing a market shift. Demand is transitioning from traditional “imaging observation” toward “high-definition imaging” and “intelligent assistance.”

Presented below is an in-depth analysis of the endoscope market in China for 2025.

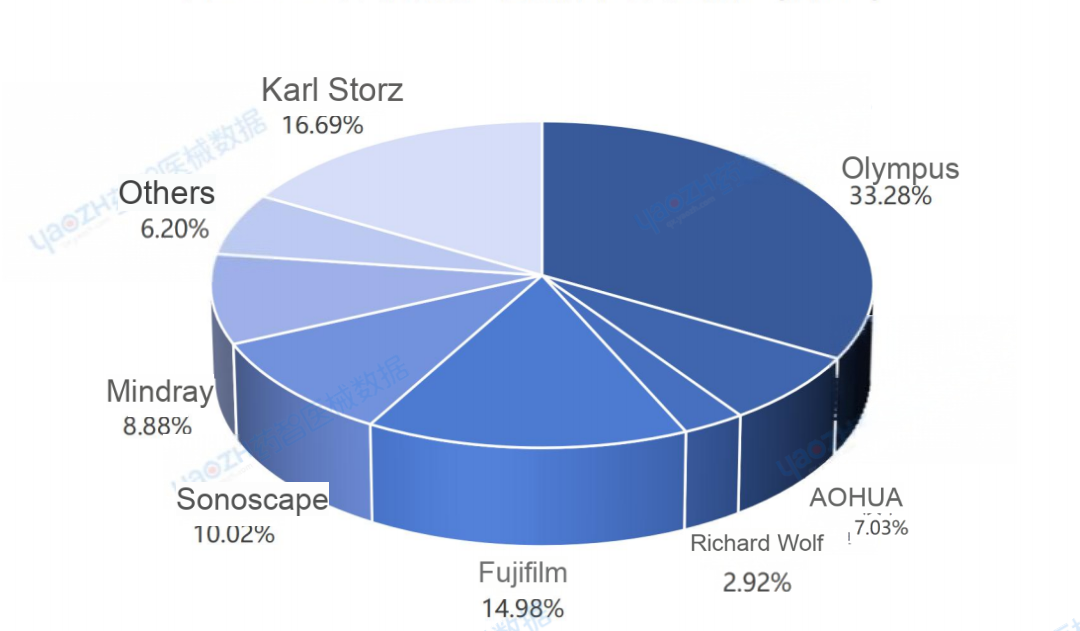

According to data, there were a total of 14,281 public tender announcements for endoscopes in China in 2025. The procurement volume reached 51,121 units/sets/batches, with a total sales value of 40.822 billion RMB. These activities covered 3,697 purchasing entities and 3,968 winning bidders. The market share by major brands is as follows: Olympus (33.28%), Karl Storz (16.69%), Fujifilm (14.98%), Sonoscape (10.02%), and Mindray (8.88%). Notably, the top three brands collectively account for 64.95% of the market.

Figure 1: Market Share of Major Endoscope Brands in China by Sales Volume, 2025

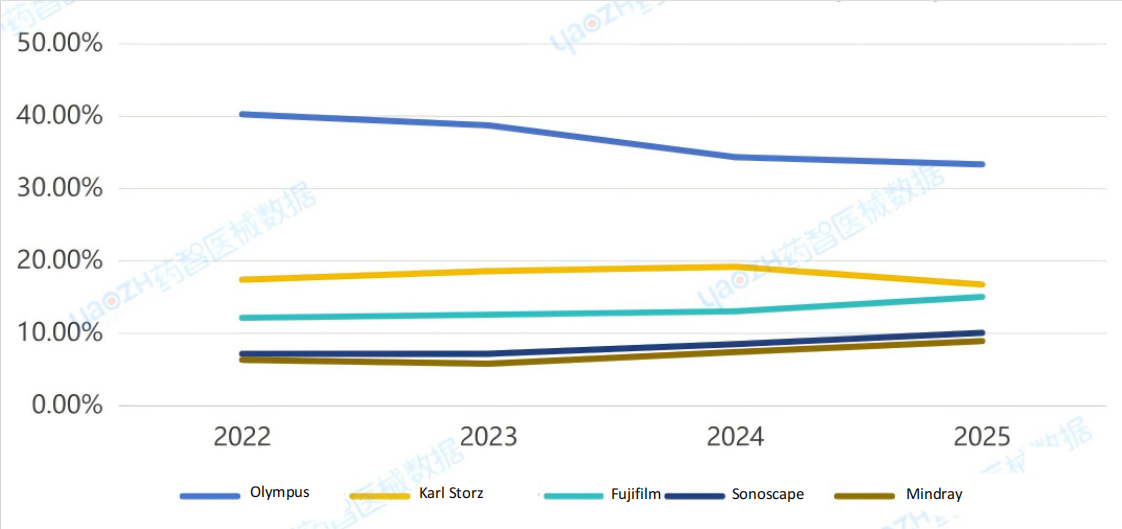

Figure 2: Market Trends of Top 5 Endoscope Brands in China (2022-2025) by Sales Volume

2.Market Overview by Endoscope Type

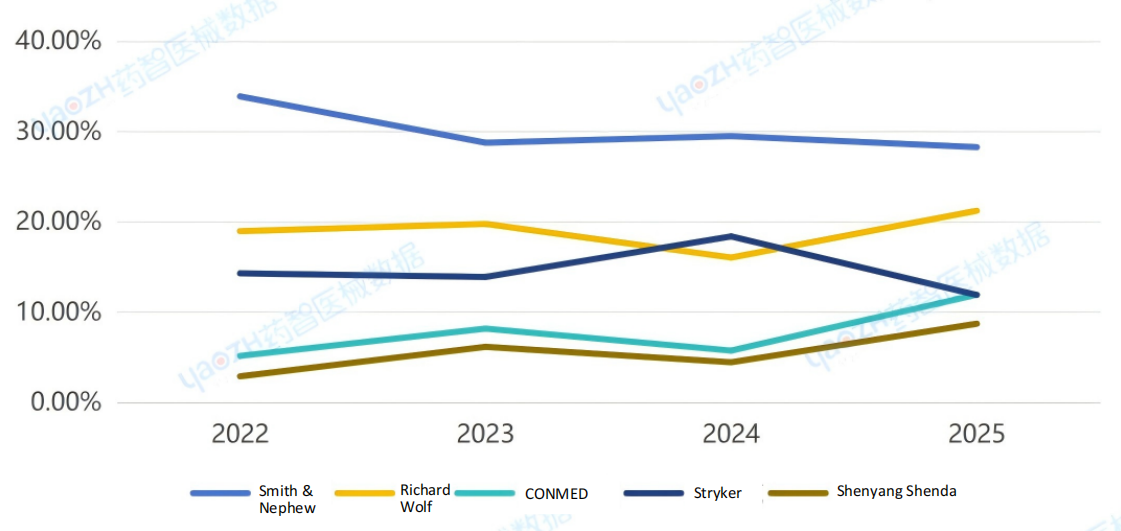

Arthroscope

The procurement volume for related equipment reached 2,399 units/sets/batches, with a total sales value of 1.752 billion RMB. The market share by revenue for major brands is as follows: Smith & Nephew (28.28%), Richard Wolf (21.23%), CONMED (11.94%), Stryker (11.91%), and Shenyang Shenda (8.72%). The top three brands collectively account for 61.44% of the market.

Figure 3: Market Trends of Top 5 Arthroscope Brands in China (2022-2025) by Sales Volume

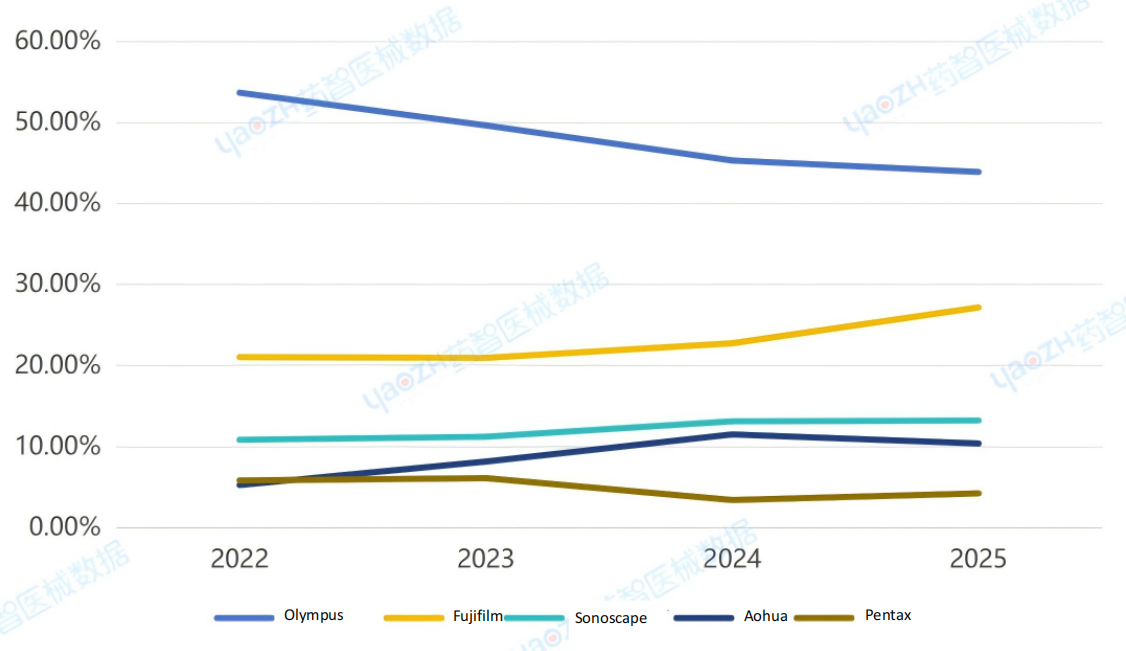

Gastroscope

The procurement volume for related equipment totaled 10,052 units/sets/batches, with a total sales value of 10.392 billion RMB. The market share by revenue for major brands is distributed as follows: Olympus (43.85%), Fujifilm (27.12%), Sonoscape (13.17%), Aohua (10.34%), and Pentax (4.18%). The top three brands collectively account for a dominant 84.14% of the market.

Figure 4: Market Trends of Top 5 Gastroscope Brands in China (2022-2025) by Sales Volume

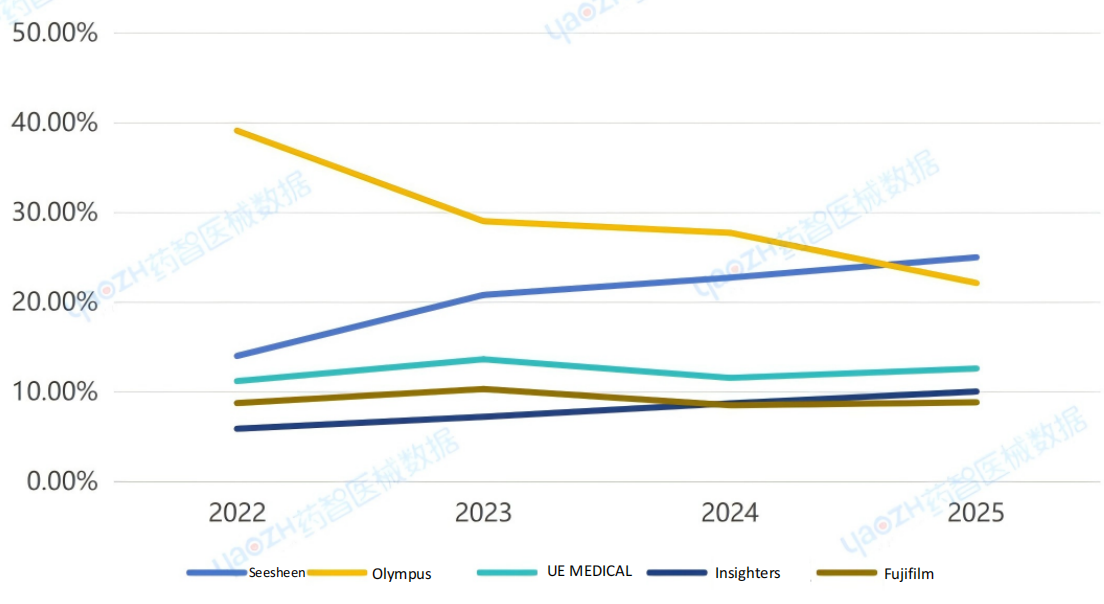

Bronchoscope

The procurement volume for related equipment reached 4,696 units/sets/batches, with a total sales value of 2.717 billion RMB. The market share by revenue for major brands is as follows: Seesheen (25.00%), Olympus (22.13%), Zhejiang UE MEDICAL (12.60%), Insighters (10.04%), and Fujifilm (8.83%). The top three brands collectively account for 59.73% of the market.

Figure 5: Market Trends of Top 5 Bronchoscope Brands in China (2022-2025) by Sales Volume

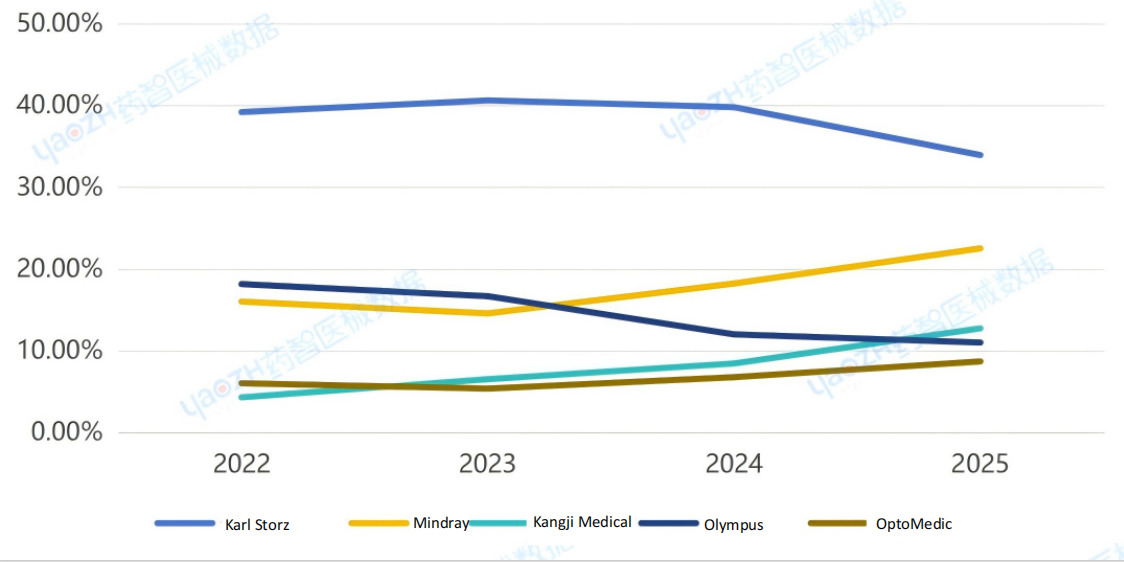

Laparoscope

The procurement volume for related equipment reached 11,750 units/sets/batches, with a total sales value of 13.125 billion RMB. The market share by revenue for major brands is distributed as follows: Karl Storz (33.93%), Mindray (22.51%), Kangji Medical (12.72%), Olympus (10.99%), and OptoMedic (8.68%). The top three brands collectively account for 69.16% of the market.

Figure 6: Market Trends of Top 5 Laparoscope Brands in China (2022-2025) by Sales Volume

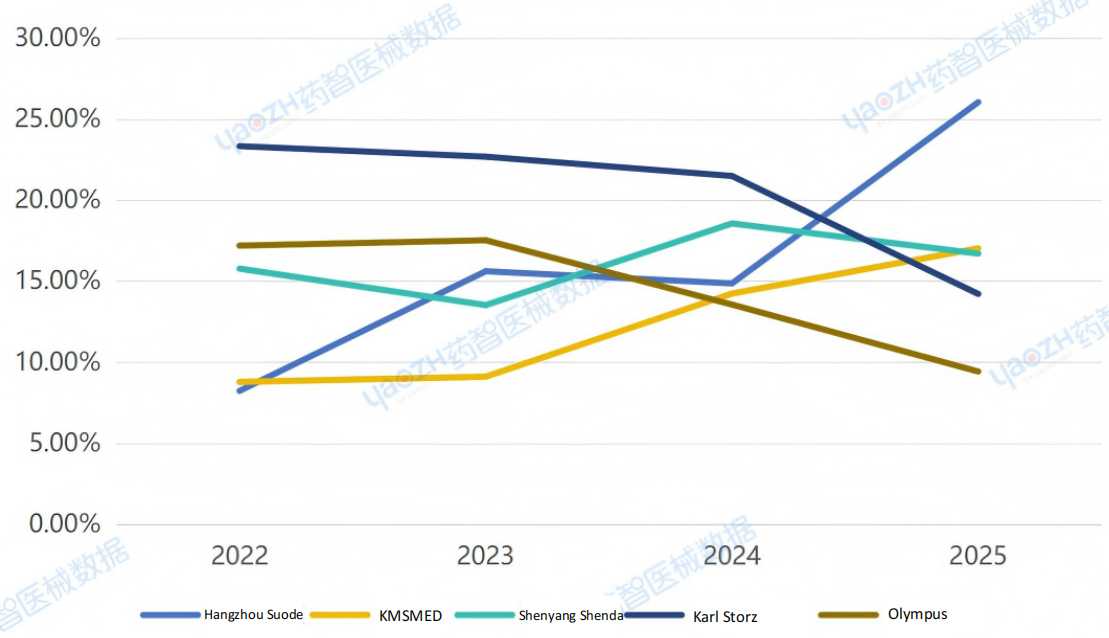

Hysteroscope

The procurement volume for related equipment reached 2,672 units/sets/batches, with a total sales value of 1.14 billion RMB. The market share by revenue for major brands is distributed as follows: Hangzhou Suode (26.04%), KMSMED (17.02%), Shenyang Shenda (16.70%), Karl Storz (14.21%), and Olympus (9.42%). The top three brands collectively account for 59.76% of the market.

Figure 7: Market Trends of Top 5 Hysteroscope Brands in China (2022-2025) by Sales Volume

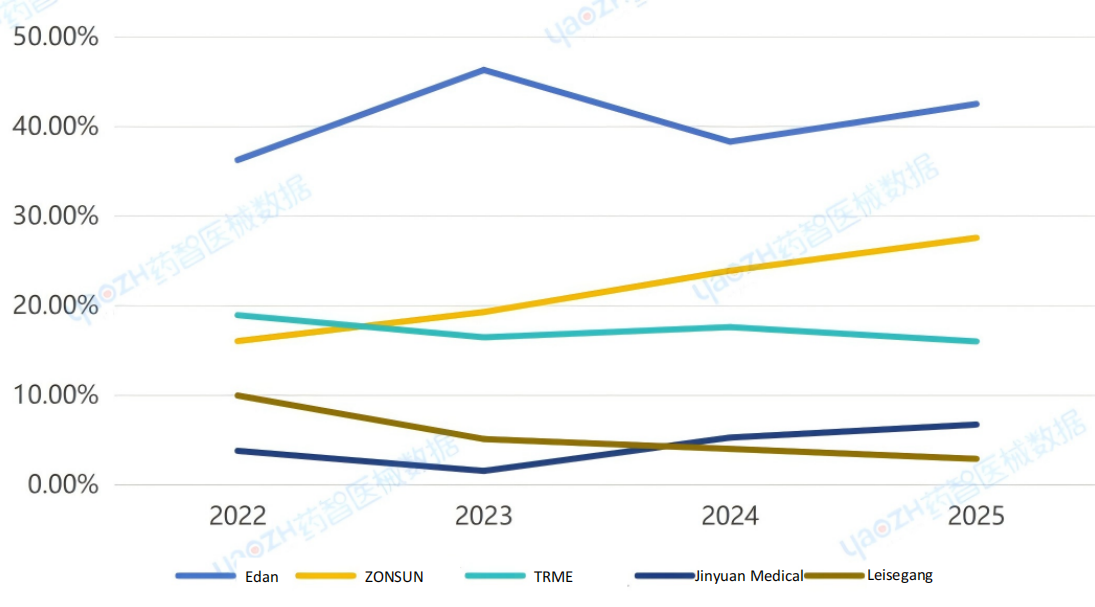

Colposcope

The procurement volume for related equipment reached 922 units/sets/batches, with a total sales value of 168 million RMB. The market share by revenue for major brands is distributed as follows: Edan (42.51%), ZONSUN (27.57%), TRME (16.00%), Jinyuan Medical (6.72%), and Leisegang (2.89%). The top three brands collectively account for 86.08% of the market.

Figure 8: Market Trends of Top 5 Colposcope Brands in China (2022-2025) by Sales Volume

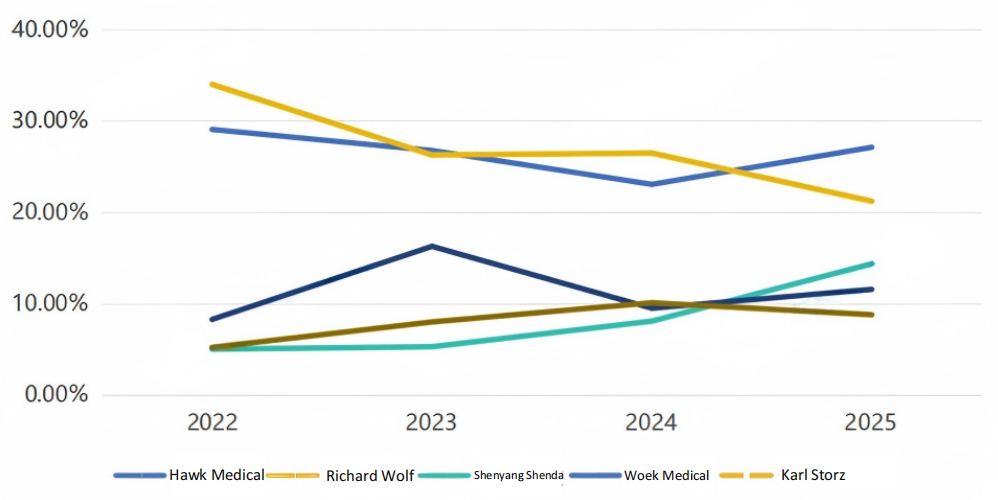

Ureteroscope / Nephroscope

The procurement volume for related equipment reached 2,948 units/sets/batches, with a total sales value of 496 million RMB. The market share by revenue for major brands is distributed as follows: Hawk Medical (27.11%), Richard Wolf (21.22%), Shenyang Shenda (14.37%), Woek Medical (11.57%), and Karl Storz (8.80%). The top three brands collectively account for 62.70% of the market.

Figure 9: Market Trends of Top 5 Ureteroscope/Nephroscope Brands in China (2022-2025) by Sales Volume

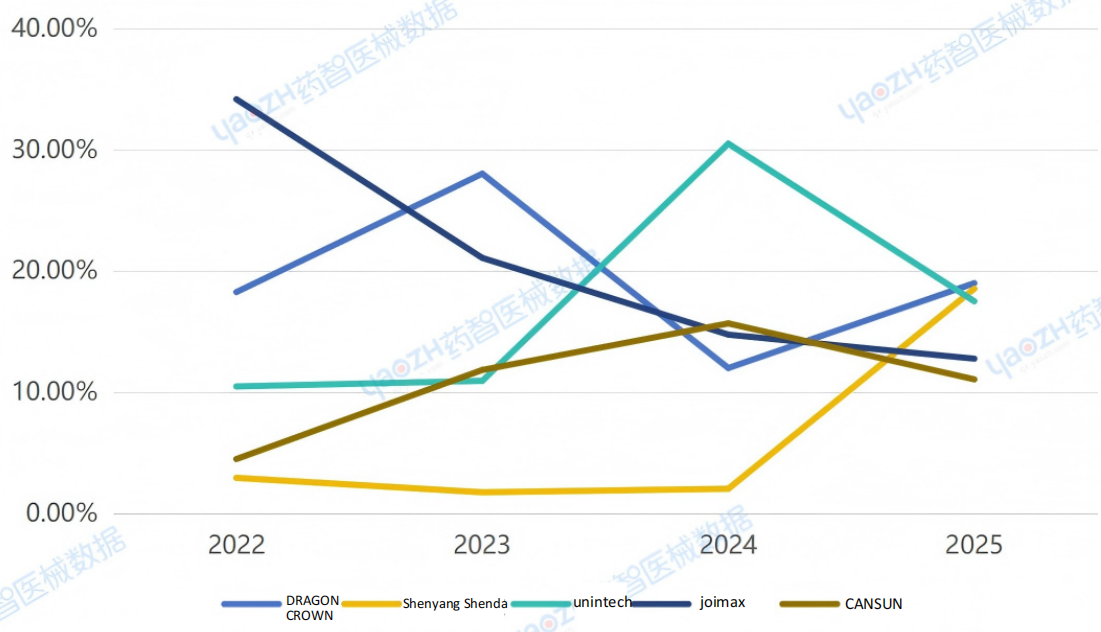

Discope

The procurement volume for related equipment reached 664 units/sets/batches, with a total sales value of 552 million RMB. The market share by revenue for major brands is distributed as follows: DRAGON CROWN (19.00%), Shenyang Shenda (18.55%), unintech (17.05%), joimax (12.77%), and CANSUN (11.06%). The top three brands collectively account for 54.60% of the market.

Figure 10: Market Trends of Top 5 Discope Brands in China (2022-2025) by Sales Volume

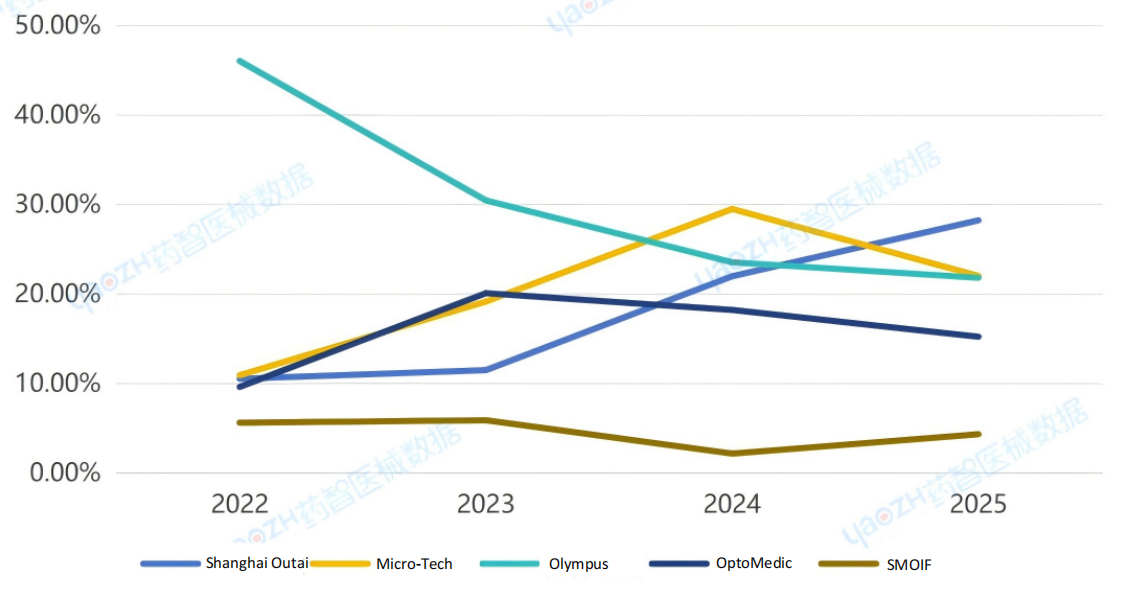

Choledochoscope

The procurement volume for related equipment reached 665 units/sets/batches, with a total sales value of 362 million RMB. The market share by revenue for major brands is distributed as follows: Shanghai Outai (28.22%), Micro-Tech (22.01%), Olympus (21.80%), OptoMedic (15.22%), and SMOIF (4.32%). The top three brands collectively account for 72.03% of the market.

Figure 11: Market Trends of Top 5 Choledochoscope Brands in China (2022-2025) by Sales Volume

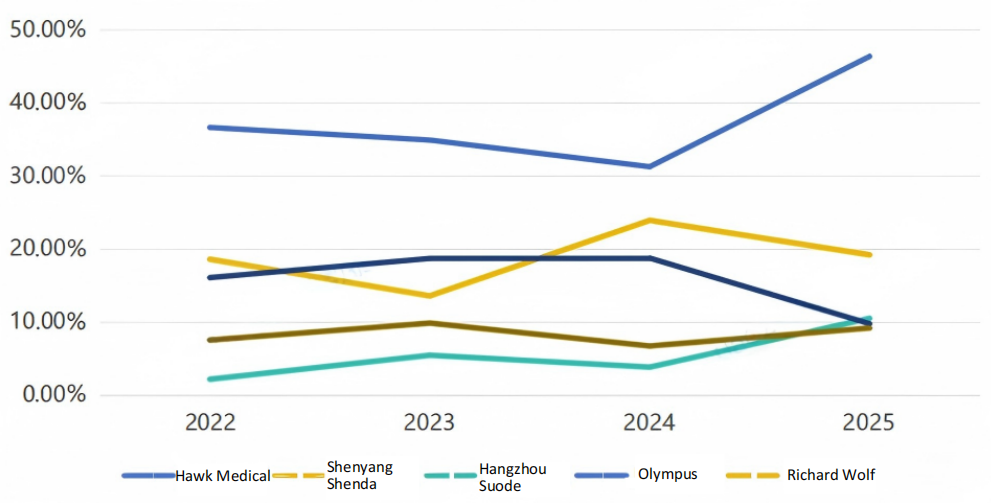

Cystoscope

The procurement volume for related equipment reached 1,045 units/sets/batches, with a total sales value of 184 million RMB. The market share by revenue for major brands is distributed as follows: Hawk Medical (46.32%), Shenyang Shenda (19.19%), Hangzhou Suode (10.51%), Olympus (9.77%), and Richard Wolf (9.19%). The top three brands collectively account for 76.02% of the market.

Figure 12: Market Trends of Top 5 Cystoscope Brands in China (2022-2025) by Sales Volume

Duodenoscope

The procurement volume for related equipment reached 433 units/sets/batches, with a total sales value of 350 million RMB. The market share by revenue for major brands is distributed as follows: Olympus (61.98%), Fujifilm (11.85%), Sonoscape (11.35%), Aohua (8.34%), and Pentax (3.86%). The top three brands collectively account for 85.18% of the market.

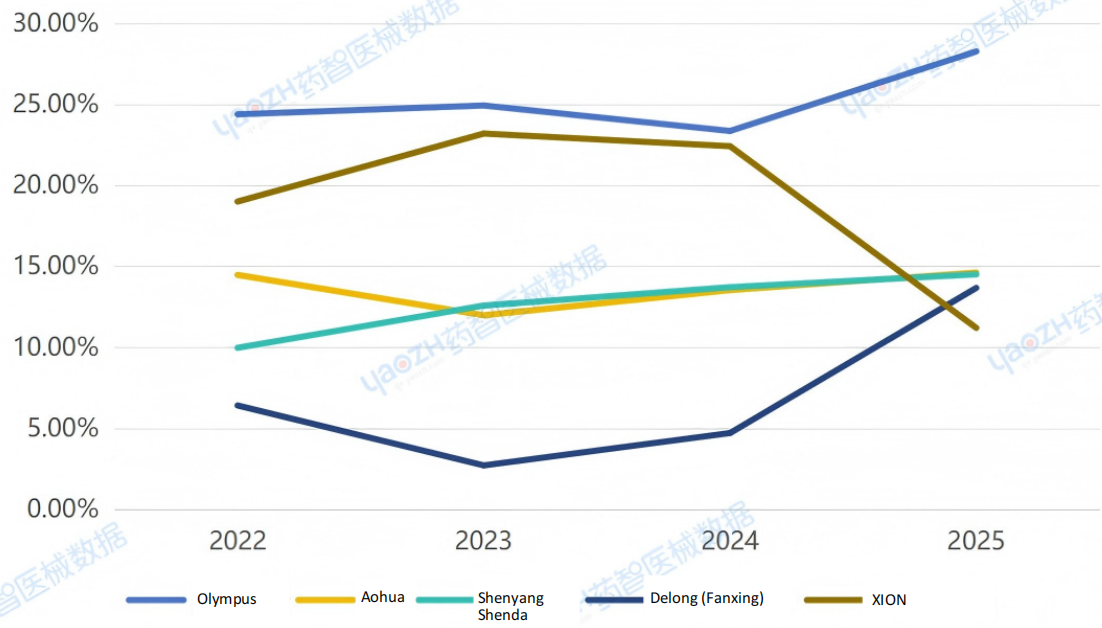

Otorhinolaryngoscope

The procurement volume for the relevant equipment was 2,566 units/sets/batches, with a total sales revenue of 1.295 billion. The market share by revenue for the major brands is as follows: Olympus (28.27%), Aohua (14.62%), Shenyang Shenda (14.51%), Delong (Fanxing) (13.67%), and XION (11.20%). The top three brands combined account for a market share of 57.40%.

Figure 13: Market Trends of Top 5 Otorhinolaryngoscope Brands in China (2022-2025) by Sales Volume

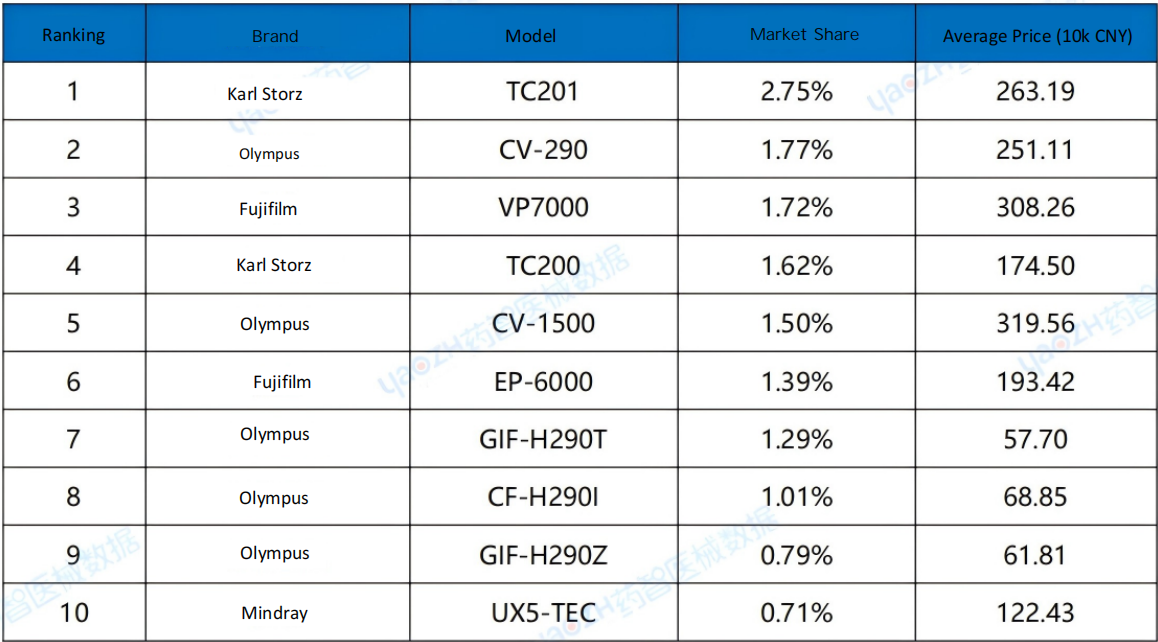

3.Product Model

Model Ranking

Olympus maintains a dominant position across all market segments. Its CV series stands out in the market, with models such as the CV-290 and CV-1500 delivering excellent sales performance.

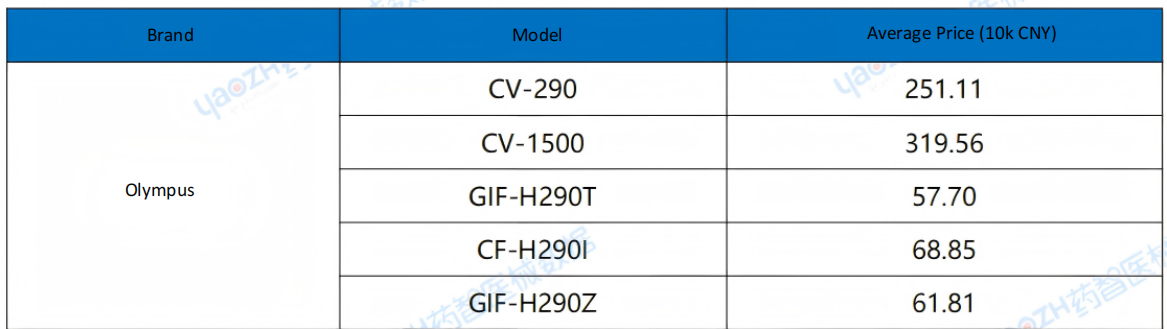

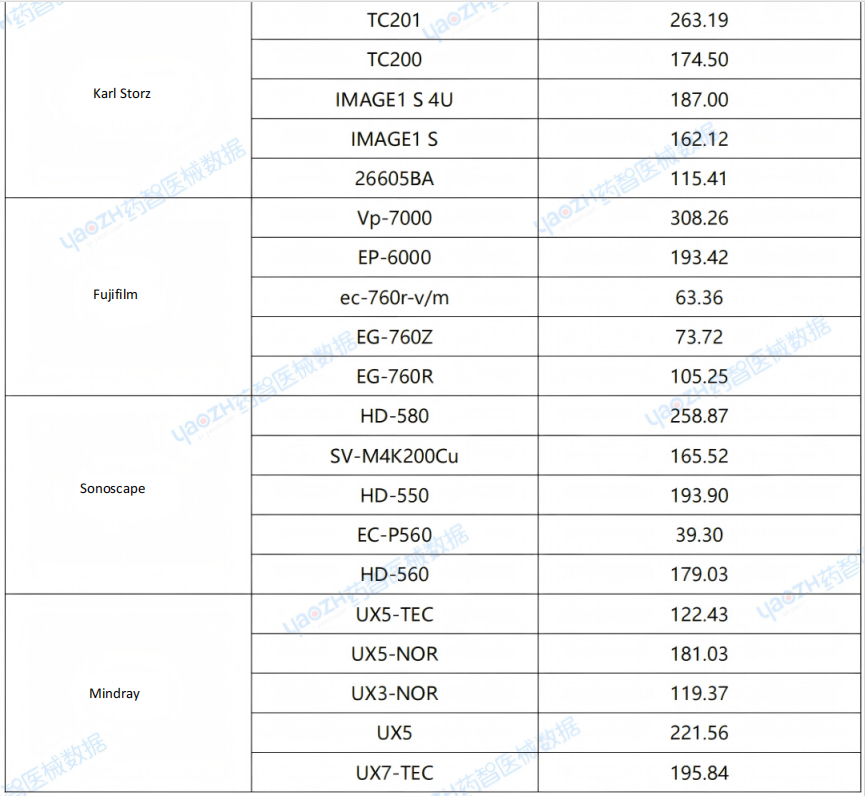

Models of Major Brands

Olympus maintains a dominant position across all market segments. Its CV series stands out in the market, with models such as the CV-290 and CV-1500 delivering excellent sales performance.

4.Purchasing Department

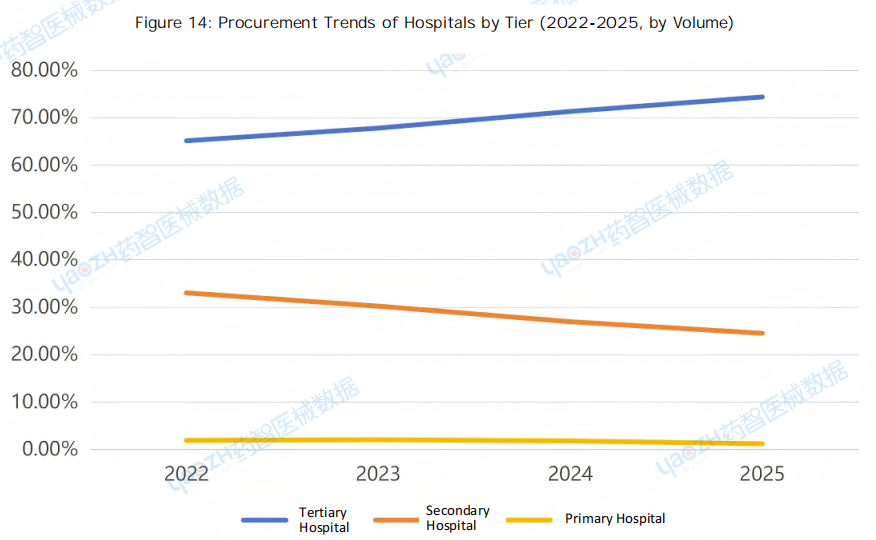

Distribution of Purchasing Units

In 2025, tertiary and secondary hospitals accounted for 74.35% and 24.48% of procurement, respectively.

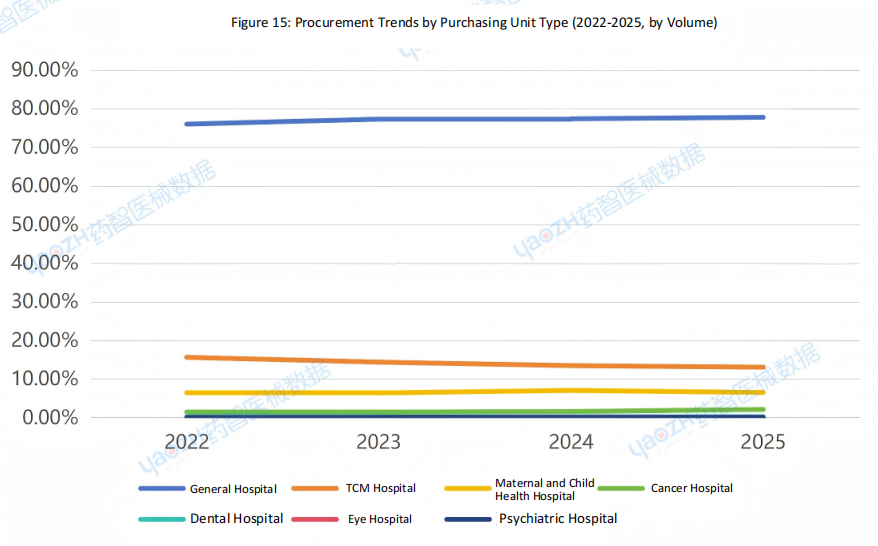

Type of Purchasing Unit

In terms of purchasing unit type, general hospitals and TCM hospitals accounted for 74.35% and 24.48% of procurement in 2025, respectively.

5.Region

Regional Distribution

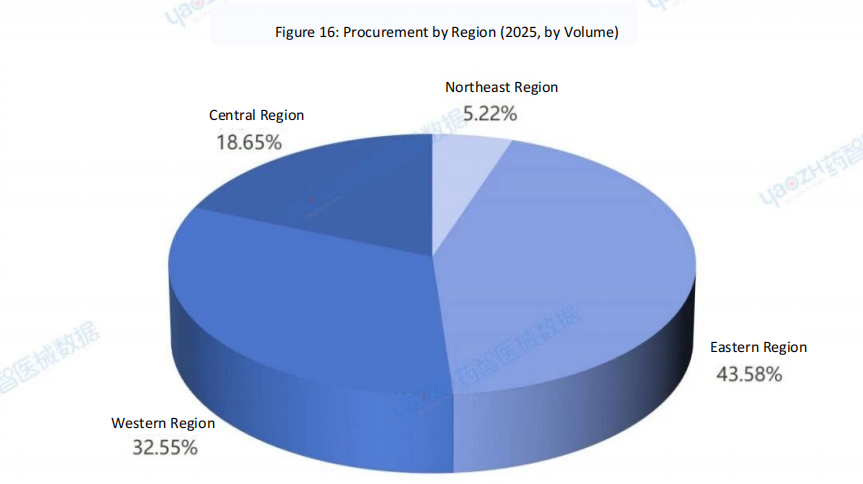

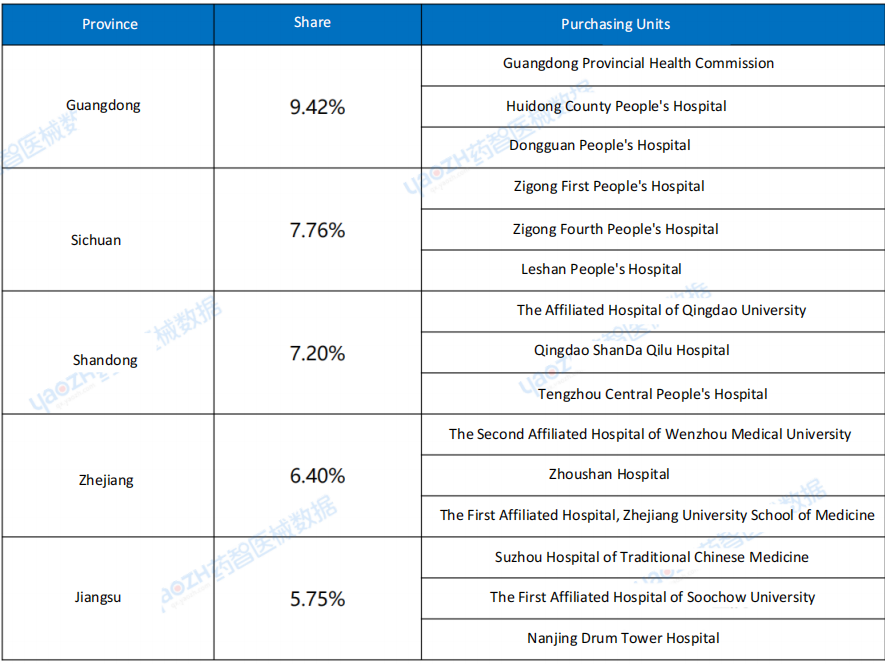

In 2025, the Eastern region accounted for the largest share of procurement volume at 43.58%, followed by the Western region at 32.55%. Figure 16 illustrates the procurement distribution across regions. In terms of provinces, the top five are Guangdong, Sichuan, Shandong, Zhejiang, and Jiangsu.

Dominant Brands by Province

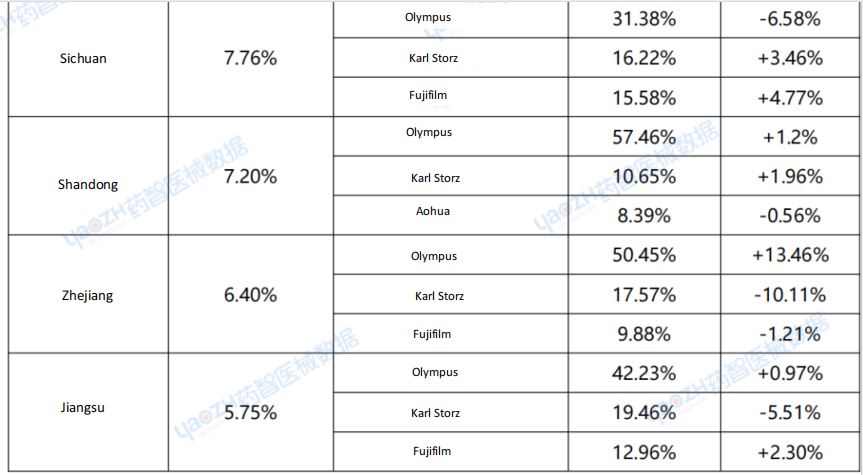

In terms of brands by province, the top five provinces are dominated by Olympus and Karl Storz.

Major Purchasing Units by Province

6.Summary

In 2025, China’s endoscope market is defined by three key characteristics: market concentration among top players, the rise of domestic brands, and the decentralization of resources.

Total annual procurement reached 40.82 billion yuan. The market is dominated by three major foreign giants—Olympus, Karl Storz, and Fujifilm—which collectively hold a 65% market share, maintaining a monopoly in high-end sectors like gastroscopes and duodenoscopes. Meanwhile, domestic champions like Sonoscape and Mindray have achieved breakthroughs in niche segments such as laparoscopes and colposcopes, surpassing foreign competitors in certain areas.

Driven by the deepening of new healthcare infrastructure policies and the “Thousand County Project,” the market is accelerating towards high-end, intelligent, and localized solutions. Going forward, technologies like 4K ultra-high definition, 3D imaging, and AI-assisted diagnosis will become standard features. It is projected that between 2026 and 2027, the aggregate market share of domestic brands will exceed 35%. Furthermore, demand from county-level hospitals and primary care institutions will continue to be unleashed, serving as a new growth engine for the market.

It is recommended that enterprises strengthen technological innovation, focus on clinical pain points, and accelerate the intelligent upgrading of products; investment institutions should pay attention to the window of opportunity for domestic substitution and lay out the construction of grassroots channels; medical institutions should comprehensively evaluate equipment performance, service support and full life cycle cost, and scientifically formulate procurement plans.

At ZRHmed, we don’t make endoscopes. We make the tools that make them work – hemoclips for bleeding control, polypectomy snares for polyp removal, sclerotherapy needles for precise, endoscopic delivery, cleaning brushes for thorough cleaning etc.

While the giants compete for the headlines, we focus on what we do best: delivering reliable, CE-marked and FDA 510 Approval accessories to distributors worldwide.

Because a great procedure needs more than a great scope. It needs great accessories.

Post time: Apr-22-2026